Many in retirement are travelling comfortably, with three key factors contributing to their happiness – good physical and mental health and enough money to enjoy life.

Perhaps the assumption that markets are still anchored by predictable economic policies needs to be challenged. For the first time since the fall of the Berlin Wall, political volatility – once background noise – is potentially reshaping investment risk at a structural level.

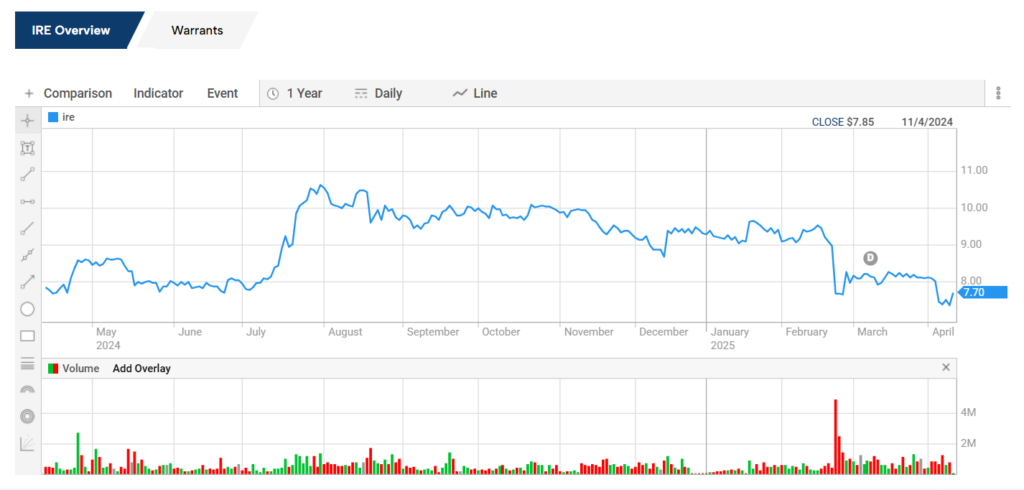

Long-suffering Iress shareholders get shot in the arm with 10c dividend

For Iress (ASX:IRE) shareholders, first the good news. The markets software group reinstated its dividend with a final payment of 10 cents a share (25 per cent franked), while establishing a target dividend payout range of between 50 and 70 per cent of NPATA (net profit after tax and before amortisation) going forward.

In rewarding shareholders after announcing a much healthier result for the year to December 31, 2024, the Iress board drew a line in the sand by announcing a more shareholder-friendly capital management strategy.

It was long overdue, because the bad news is that the Iress share price has gone backwards over the past five years. A stock that was trading at $10.54 in April 2020 closed on Tuesday at $7.79 – a 26 per cent decline. Over a 12-month horizon, the strong gains over the first three months – it closed at $10.63 on July 31, 2024 – have been handed back over the past nine months.

What Iress’ long-suffering shareholders must be hoping for is that the full-year result is a sign of better things to come, and that it is finally positioning itself for a period of sustained growth and improved shareholder returns.

Certainly, the numbers had a rosier hue about them with a 25 per cent increase in adjusted earnings before interest, tax, depreciation and amortisation (EBITDA) to $132.8 million. This improvement came alongside substantial margin expansion, with the adjusted EBITDA margin rising by more than 500 basis points, to 22 per cent.

In a message to shareholders, chief executive officer Marcus Price (pictured) highlighted the company’s transformation into “a simpler, leaner business focused on driving operating leverage and building growth vectors”.

“Having made the clear strategic choice to focus on our strong key businesses, we are well-positioned to capture the significant opportunities present in global wealth management, powered by data and AI, while continuing to provide critical trading and market data infrastructure to the industry.”

A central element of Iress’ transformation has been divesting non-strategic assets to focus on its two core businesses: trading and global market data and wealth management. This streamlining effort included selling businesses such as Mortgages UK, Platform, Managed Funds Admin, and, most recently, the sale of its superannuation business to Apex Group, expected to be completed before June 30.

The company’s continuing business operations in the 2024 financial year delivered four per cent revenue growth, while simultaneously achieving a two per cent reduction in operating expenses – a notable achievement in an inflationary environment. Chief financial officer Cameron Williamson pointed to a 15 per cent reduction in overall full-time employees as central to this cost discipline.

Perhaps most impressive was the 39 per cent increase in adjusted EBITDA across continuing business units, demonstrating that the strategic concentration is already delivering substantial operational leverage.

Looking ahead to the 2025 financial year, Iress has provided guidance of adjusted EBITDA of between $127 million and $135 million (representing six to 12 per cent growth) and NPATA of between $54 and $62 million (a substantial 80-106% increase over 2024).

The company is betting on several strategic priorities across its two core businesses. In trading and global market data, where Iress holds pole position in Australia and the UK, the focus will be on technology modernisation supporting inter-operability and cloud solutions; enhanced APIs and global connectivity through expansion of its FIX Hub; responding to market demand for data-driven trading solutions; and upgrading its buy-side EMS and IOS+ offerings for ASX Service Release 15.

In wealth management – it’s number one in Australian and number two in the UK – the priorities include capitalising on regulatory tailwinds and unmet advice needs; developing digital advice solutions for superannuation; expanding Xplan’s capabilities, particularly in retirement income planning; building strategic partnerships to expand its ecosystem; and growing data product revenues.

It all sounds promising. But long-time shareholders might say they have heard it all before. They would also remember that their board has turned down two private equity offers in the belief that an internal reset would optimise shareholder value. Well, there’s no arguing the reset is occurring – just not fast and far enough yet to convince sceptical investors.