Many in retirement are travelling comfortably, with three key factors contributing to their happiness – good physical and mental health and enough money to enjoy life.

Perhaps the assumption that markets are still anchored by predictable economic policies needs to be challenged. For the first time since the fall of the Berlin Wall, political volatility – once background noise – is potentially reshaping investment risk at a structural level.

Geopolitical fallout sparks a share market revival in Germany

Self-funded retirees have learnt a valuable lesson in recent months – diversifying their portfolios overseas is not just a US story.

While the fallout from President Donald Trump’s inane tariff policies are yet to be seen in the wake of Liberation Day, the reality is that this administration is committed to this policy, having already imposed tariffs on goods from Canada, Mexico and China, steel and aluminium imports, and foreign cars and auto parts.

No serious economist doubts this policy, if executed in full, will push inflation up in the US as higher prices flow into the economy, possibly tipping the US into recession (tariffs are taxes on imports that companies typically pass on to customers). Stagflation is even being mentioned. Certainly, investors think so with both the Dow Jones and S&P 500 bellwether US share market indexes down.

All this, and just two and a half months into Trump’s presidency. Little wonder analysts globally are beginning to question US exceptionalism that has prevailed for the past decade and is best symbolised by the Mag 7 – Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla – that account for about one-third of the S&P 500’s total market value.

Since then, however, Seema Shah, chief global strategist at the global investment management group, Principal Asset Management, says three factors have coincided to test the US exceptionalism theme.

“The US technology sector – the primary driver of its equity market performance in recent years – has been significantly challenged as investors question stretched valuations and earnings expectations.

“Growth expectations for the US economy have been revised downward in response to rising policy uncertainty, and policy proposals that have proven to be more severe than widely expected.”

But it’s the third theme that could interest investors – the hopes for a broader European fiscal shift. It has begun in Germany where the Bundestag (Germany’s parliament) has passed a landmark spending package that promises to unlock almost one trillion euros for defence and infrastructure, ending decades of budget austerity.

If Germany’s decision marks the beginning of a European fiscal trend that’s a direct response to the geopolitical uncertainty created by the Trump administration – the Ukraine conflict has become its flashpoint – then investors might consider a European play.

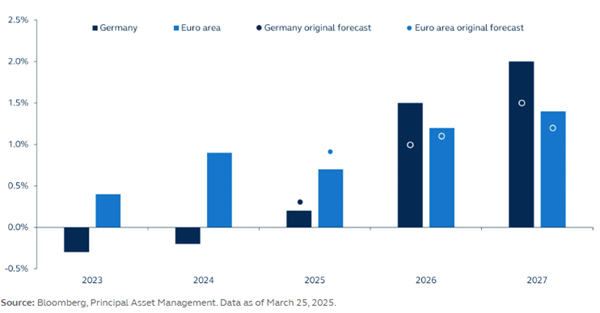

Revised forecasts: Expected impact on Germany’s growth outlook (2023–27)

Certainly, the German market has responded with the DAX stock market index – it consists of the 40 major German blue-chip companies trading on the Frankfurt Stock Exchange – up 10 per cent this calendar year. It closed on Tuesday at 22,540.

The German response has been dramatic with the government changing its constitutional rules, ushering in the following initiatives: the creation of a €500 billion ($860 billion) infrastructure investment fund; exempting defence spending above one per cent of GDP from the ‘debt brake’ rule (a rule introduced in 2009 by former Chancellor Angela Merkel under which the federal government must limit annual borrowing to 0.35 per cent) of GDP; and easing fiscal constraints for the federal states.

As Shah says, taken at face value, Germany is set to embark on a major fiscal expansion – with the €1 trillion ($1.7 trillion) – far exceeding expectations.

“While a policy shift wasn’t a surprise, the scale marks the biggest change in Germany’s fiscal approach since reunification 35 years ago. The reforms could raise allowable structural net borrowing by more than two per cent of GDP annually, though questions remain about how quickly the funds can be deployed,” said Shah.

Germany’s planned fiscal expansion remains uncertain in timing and composition, but its scale suggests lasting economic impact. While the effects will take time to materialise, and US tariff threats pose headwinds, near-term growth in Germany is likely to remain weak – although slightly improved from recent trends.

“We do expect the German economy, after two consecutive years of contraction, to grow by 0.2 per cent this year,” says Shah.

“However, once the fiscal impulse kicks in, the impact to economic growth will be significant, providing an estimated 0.5 per cent boost to German GDP growth over the next few years. We expect Germany’s economy to grow by 1.5 per cent in 2026 and two per cent in 2027.

“If the infrastructure investment is paired with structural reforms like deregulation, Germany’s fiscal shift could lift productivity and support long-term growth near two per cent – similar to that of the US.”

Remember, too, that Germany makes up about a third of Euro-area GDP, so its fiscal expansion will lift Europe.

“At the same time, the EU has proposed a modest but supportive fiscal shift, including looser budget rules to enable more defence spending, a “national escape clause” for member states, and a new €150 billion ($258 billion) loan facility to support investment,” says Shah.