When Federal Treasurer Jim Chalmers hands down the budget on 14 May, the pressing need for fiscal responsibility is likely to trump spending programs.

In an era of fake news, it’s getting more difficult to separate fact from fiction. Yet it’s imperative we do so because the consequences for being deceived can be enormous.

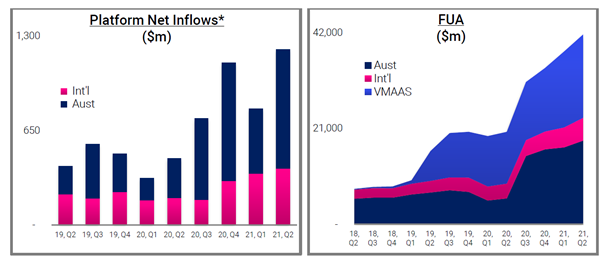

Platform space is heating up as net inflows continue to grow

If you’ve been watching or own shares in the wealth platform space, you’d be punching the air in delight as the three innovative new generation platforms hit record highs amid a sea of consolidation and disruption.

Netwealth and HUB24 are often labelled as the original pioneers of disruption as they began to threaten the status quo, offering ‘more for less’ than the big four banks. Following on from the Royal Banking Commission, a record number of advisers shifted towards non-aligned financial advice, away from a vertically integrated banking world. The shift was led by the consumer, driving advisers to platforms that better suited their client’s needs.

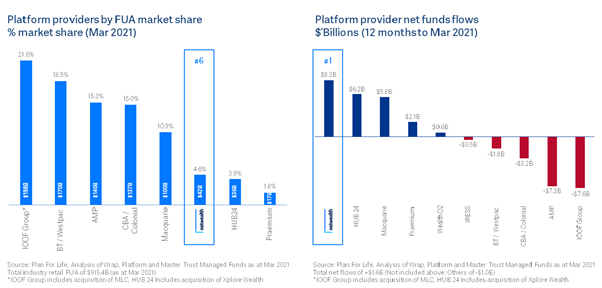

The platform space is made up of six main banking platforms that represent the bulk of the funds under administration. The next five investment platforms are the disruptors that continue to be engorged by the massive inflows stemming from post Royal Banking Commission to put an end to misconduct. The final group are seven start-up platforms that that are in their early days of the next disruptive tech wave.

The bank platforms continue to see negative funds under advice numbers with their stranglehold evaporating at a rapid rate. If IOOF completes its takeover of NAB’s MLC Wealth it would become the market leader but as you can see below gone are the days when AMP ruled supreme. Here is the platform break up:

The shift towards non-aligned platform advice forced structural change within the wealth management industry that was long overdue. It helped drive the push towards independent platforms and product providers because of their renewed client focus. The “original fintech” platforms such as Netwealth and HUB24 were the innovators that led the movement of advisers away from bank platforms into the now highly competitive area.

There are three original fintech leaders reporting massive gains in quarterly net inflows. The three are Netwealth (ASX:NWL), HUB (ASX:HUB), and Praemium (ASX:PPS) in market capitalisation order.

Netwealth (ASX:NWL) – Is the champion of the original fintech’s when going by Funds Under Administration. Year after year, the platform wins the Investment Trends 2020 Platform Benchmarking & Competitive Analysis Report and various other reports as the overall preferred platform going by functionality and adviser preferences. However, it’s always a tight race because HUB24 is only centimetres behind or it takes top spot. HUB24 beat Netwealth for top spot in the latest report.

- HUB24 (overall score of 89.0%)

- Netwealth (88.9%)

- Praemium (84.8%)

- BT Panorama (82.4%)

- Macquarie Wrap (76.5%)

Netwealth is considered to be the leading tech platform at the moment servicing both wholesale and retail advisers. It released its June quarter highlights last week. The platform posted a FUA of $47.1bn up 12.7% ($5.3bn) from the prior period. FUA net inflows of $3.1bn for the June Q together with market movements of $2.2bn. The platform retains its #1 position in the industry for overall satisfaction for the 9th year in a row, according to Investment Trends, June 2021 Planner Technology Report. NWL has a market share of 4.6% and is 7th largest platform in Australia.

In terms of the brokers, Credit Suisse has an Underperform recommendation with a target price of $16.50. The broker is a little cautious on Netwealth saying it faces the likelihood of being disrupted or negative headwinds from M&A from the larger platforms as well as tougher regulations.

HUB24 (ASX:HUB) on the other hand, is more of a retail platform servicing mum and dad advisers. The retail platform released its Quarterly results this week, which were well received. HUB posted net inflows of $3.9bn, resulting from the HUB platform, acquisitions of ClearView Wealth and Xplore Wealth. In total HUB recorded a whopping $58.6bn in FUA up 141%, lifting the platform above Netwealth.

There are 5 Broker Buys on HUB.

- Credit Suisse has an Outperform recommendation with a target price of $31.50. HUB is gaining share with NWL and stands to benefit from significant disruption in the industry. The broker says, “this will stem from sale processes, de-mergers and integrations at large institutional platforms, as well as the ban on grandfathered commissions which came into effect on January 1, 2021.”

- Ord Minnett has a Hold recommendation with a target price of $16.00. The broker has labelled NWL’s quarterly update as ‘a very good one’. Ords expects this momentum to continue given the massive market opportunity. Modest upgrades were made to forward forecasts.

And that leaves us with Praemium (ASX:PPS), the underdog that managed to leapfrog into third place late last year. Praemium achieved this significant growth via its takeover of Powerwrap. It helped the platform fly up the ranks to be on an equal footing with Netwealth and HUB24.

With a $1.4 billion portfolio in alternative assets across 350 funds and a predominantly high/ultra-high-net-worth client base, Powerwrap was a natural fit for Praemium given its top ranked Managed Accounts Product offering, and its next-generation investment portfolio reports. Praemium doubled profit, increased FUA to $27 billion. Posted a record quarter with June Q inflows of $1.2bn taking FUA to $41.7bn. Australia platform FUA of $18.4 billion, up 223% in the 2021 financial year on reported FUA and up 30% for the consolidated Praemium and Powerwrap.

The International platform (FUA of $5.0bn up 55%) was put up for sale this week, shares rising 10%. The announcement comes after the eyebrow-raising May departure of chief executive Michael Ohanessian, who was previously dismissed by the company’s board in 2017 before being reinstated with the support of investors including Australian Ethical and David Paradice. Non-executive director Anthony Wamsteker has since taken on the role of interim CEO.

- Ord Minnett has a Buy recommendation with a target price of $1.40. The broker says it was a record quarter of net flows and strong momentum in all three businesses. Still question marks over the sale price on the international business. Ords says “a successful sale will increase the attractiveness of the Australian business to a domestic suitor”.

So, the decision of who to buy?

In a rising interest rate environment, all three of these three platforms tick all the right boxes and should continue to do well in the short term supported by a thematic tailwind. The two pioneers, Netwealth and HUB24 successfully disrupted a space that once tightly held by the big banks. Each platform has its niche offering and appeals to that market in a unique way.

However, all three are facing a wave of disruption from AI based platforms that offer cheaper administration, and better pricing on cash, are more nimble, and have the backing required to grow and disrupt this industry.

Kevin Chidgey from UBS released a report titled Australian wealth management, the next wave of disruption which pointed to a new wave of wealth management platforms that had the ability to reduce admin fees as low as 7 to 12 basis points offering above RBA rates for cash holdings as the likely catalyst for further cost reductions. He picked startups such as Findex’s Centric, Spitfire, and FinClear as three to lead the next disruption wave of platform providers.

Praemium is the pick

At present, there is no ‘one size fits all’ platform that effectively accommodates all types of advisers/customers nor is there a platform that offers the service free of charge to dealer groups and financial advisers.

For a service that doesn’t add significant value, platforms are clunky, slow and force advisers to pay excessive fees. The level of satisfaction financial advisers have with their main platform is falling at a faster than ever rate. Investment Trends’ latest Adviser Technology Needs Report showed only 28% of advisers rated their overall satisfaction with their main platform as ‘very good’.

With this in mind, we think the platform space is a short-medium term play. Praemium is the most attractive of the three because we think it is a potential takeover target. With the sudden exit of chief executive Michael Ohanessian and the International Business gone, the board is in control. It leaves the door right open for an international player to swoop up the entire business. The sudden exit of a CEO who built such a formidable business and successful merger with Powerwrap should have seen its shares tumble.

Instead, shares are up almost 20% in a week. Even with this movement taken into account, Praemium is trading at a huge discount to the other two players. Takeover or not, shares are attractive at current levels according to most experts.