Many in retirement are travelling comfortably, with three key factors contributing to their happiness – good physical and mental health and enough money to enjoy life.

Perhaps the assumption that markets are still anchored by predictable economic policies needs to be challenged. For the first time since the fall of the Berlin Wall, political volatility – once background noise – is potentially reshaping investment risk at a structural level.

Self-funded retirees urged to hold fast to investment strategies

The global market turbulence sparked by “Liberation Day” would have some self-funded retirees pondering whether to increase their cash holdings – a knee-jerk reaction that advisers strongly warn against.

Link Wealth managing director Stephen Sloane is quite emphatic on how investors should respond – stay the course with their chosen investment strategies.

“What’s happening at the minute (in the markets) can be quite short-term and reacting to it could have big consequences for portfolios. It’s all about getting the asset allocation correct and taking a medium to long-term view rather than focussing on short-term media releases,” he tells The Golden Times.

“Clearly, we have a situation in the US where there are going to be new headlines frequently hitting the papers and investors have to be aware that there will be market reactions to that – and it’s likely to be more frequent than what we have seen in the past.”

Sloane is right about market volatility. Since “Liberation Day” was announced on April 2, the two bellwether US share market indexes, the Dow Jones Industrial Average and the S&P 500, are down 10.8 per cent and 12 per cent, respectively. With a 20 per cent decline for a sustained period heralding a bear market, little wonder investors are skittish.

In Australia, the fall is less dramatic with the S&P/ASX 200 index down 3.7 per cent since April 3, having clawed back 2.3 per cent on Tuesday with the market appreciating renewed speculation about interest rate cuts.

Wattle Partners principal Drew Meredith is on the same page as Sloane in counselling retirees to hold their nerve, arguing that now is likely to be the “worst time” to increase cash holdings in a portfolio.

“These sorts of corrections and volatility are the price of admission for investing in share markets, and if your initial reaction is wanting to sell, then your portfolio is likely not appropriately suited to your tolerance for risk and volatility, or you didn’t truly understand where you were investing.

“Similarly, this also isn’t a time to immediately buy more shares for your portfolio, as these periods of difficultly can last for an extended period.”

Meredith says periods like this are why Wattle Partners seeks to build “resilient” portfolios, diversified across multiple asset classes and income streams, some of which may have under-performed when the share market was doing well in 2024.

“In a market where everything has gone up for several years, every investor thinks they’re ‘doing it pretty well themselves’ – until circumstances change and normal market conditions emerge.”

Arguments to stay the course with an investment strategy is not to say that self-funded retirees shouldn’t actively seek the best possible returns for their cash and term deposits. After all, at December 31, 2024, SMSFs held $161 billion in this asset – 16 per cent of this super sector’s total net assets of $981 billion – so they would be remiss not to do so.

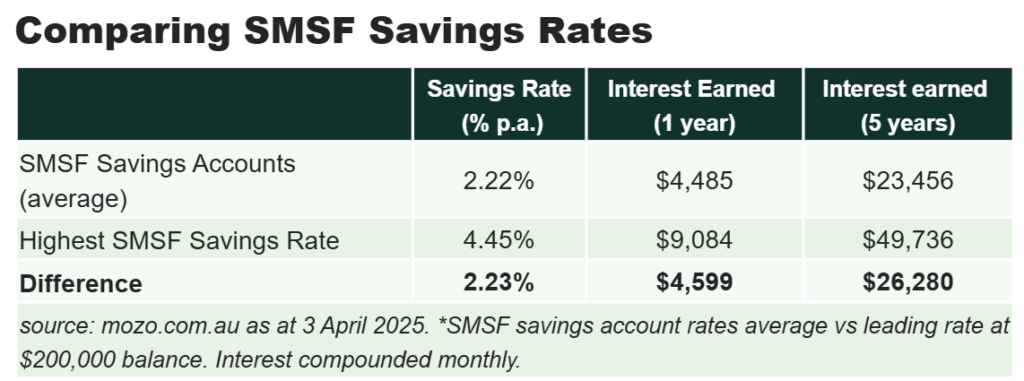

According to the financial comparison site Mozo, analysis reveals “sleepy” SMSF savings rates could cost account-holders thousands of dollars in annual interest.

Mozo’s Rachel Wastell (pictured) says comparing 35 SMSF savings accounts found a 2.23 percentage-point difference in savings rates between the average rate and the highest rate on offer.

“Looking at a one-year period, settling for the average rate of 2.22 per cent a year instead of opting for the highest rate of 4.45 per cent a year could cost $4,599 in annual interest on a $200,000 SMSF cash balance,” she says.

“Even opting for the third-highest rate of 4.35 per cent a year rather than settling for the standard could lose SMSFs $4,391 in annual interest.”

Over five years, securing the best SMSF savings rate in the market adds up to more than $26,000 in additional interest when switching from the average on offer, while opting for the fifth-highest rate could get SMSF savers with a $200,000 balance an extra $21,353 in interest over five years.

“Many SMSF savers don’t realise that leaving their cash in a low-interest account could be costing them tens of thousands of dollars, as when it comes to large SMSF balances, the tiniest difference in rates really adds up,” she says.